Contents

Understanding the Basics of Accounting

Accounting is the process of recording, analyzing, and interpreting financial transactions of a business. It involves the systematic recording of financial data, such as sales, expenses, and assets, to provide accurate and reliable information for decision-making. In simple terms, accounting helps businesses keep track of their financial activities and understand their financial position.

The Importance of Accounting Principles

Accounting principles are a set of guidelines and rules that govern how financial transactions should be recorded and reported. These principles ensure consistency, transparency, and accuracy in financial reporting and help businesses maintain credibility with stakeholders, such as investors, lenders, and government agencies. By following accounting principles, businesses can ensure that their financial statements are reliable and provide a true and fair view of their financial performance.

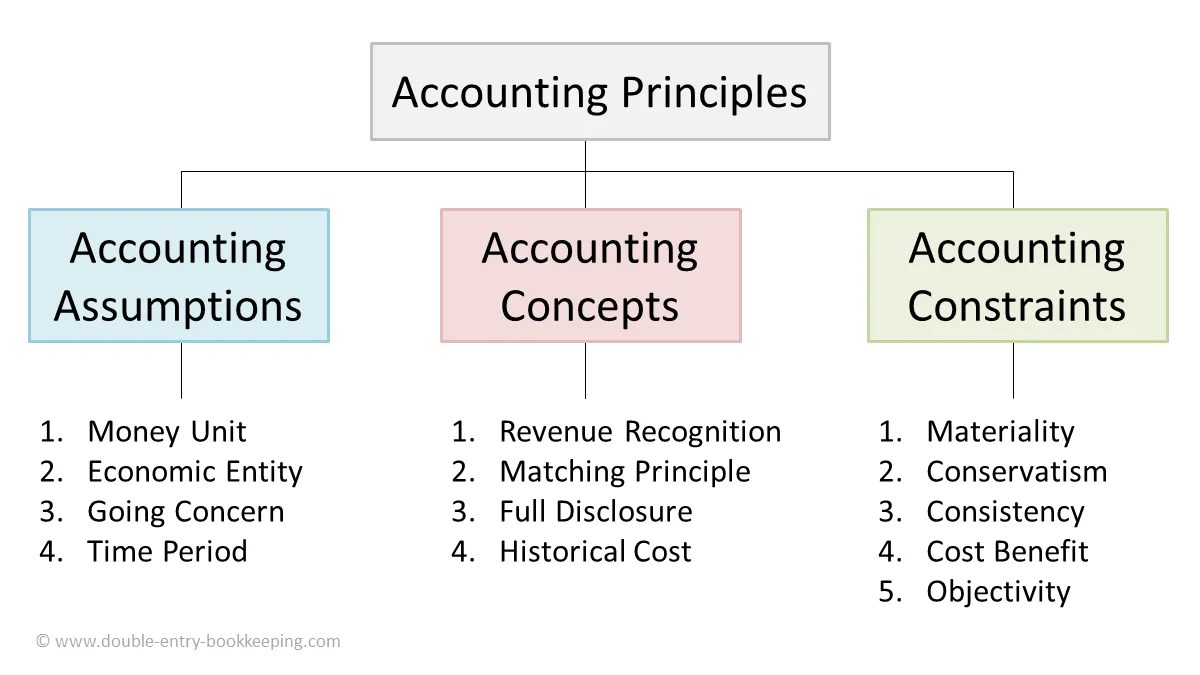

The Basic Accounting Principles

There are several accounting principles that businesses follow to ensure accurate and reliable financial reporting. These principles include:

1. The Entity Principle

The entity principle states that the financial transactions of a business should be separate from the personal transactions of its owners. This principle ensures that business assets, liabilities, income, and expenses are recorded and reported separately from the personal assets and liabilities of the owners.

2. The Going Concern Principle

The going concern principle assumes that a business will continue to operate indefinitely. This principle allows businesses to prepare financial statements under the assumption that they will continue to operate and generate revenue in the foreseeable future. It also ensures that assets are recorded at their original cost and not at their liquidation value.

3. The Matching Principle

The matching principle requires businesses to match expenses with the revenue they generate. It ensures that expenses are recognized in the same accounting period as the revenue they help generate. For example, if a business sells a product in January but incurs the cost of producing it in December, the cost should be recognized in the same period as the revenue.

4. The Accrual Principle

The accrual principle states that revenues and expenses should be recognized when they are earned or incurred, regardless of when the cash is received or paid. This principle ensures that financial statements reflect the economic reality of a business, even if cash transactions have not yet taken place. For example, if a business provides services to a customer in December but receives payment in January, the revenue should be recognized in December.

5. The Consistency Principle

The consistency principle requires businesses to use the same accounting methods and principles from one period to another. This principle ensures that financial statements are comparable over time and allow users to make meaningful comparisons and analysis. Changing accounting methods without a valid reason can lead to inconsistencies and distort the financial picture of a business.

In Conclusion

Accounting is a crucial aspect of any business and involves the recording, analyzing, and interpretation of financial transactions. Accounting principles provide a set of guidelines and rules that ensure accurate and reliable financial reporting. By following these principles, businesses can maintain credibility and provide stakeholders with a true and fair view of their financial performance.